For many Florida buyers, homeowners insurance feels like one more closing requirement. Then the deductible shows up, and it changes the real risk of owning the home.

That matters because a deductible affects two different parts of your budget. First, it can affect your premium, which shapes your monthly housing cost. Second, it affects how much cash you must have available after a covered loss. In Florida, that second issue can be much more serious because many policies include a separate hurricane deductible that may be based on a percentage of the dwelling limit, not a small flat-dollar amount, as explained by the Florida Department of Financial Services.

This guide explains how deductibles work, how Florida hurricane deductibles differ from standard deductibles, and how to choose a deductible that fits both your property and your financial reality.

Need the fastest answer? The best deductible is usually the one you can realistically pay from savings without throwing off your mortgage, repairs, or other essential bills.

Quick Start: Pick Your Path

Buying your first Florida home? Start with the sections on definitions and deductible choices.

Comparing quotes? Go to the comparison table and deductible-selection roadmap.

Living near the coast or worried most about storms? Read the hurricane deductible section carefully.

Limited emergency savings? Focus on out-of-pocket risk before choosing a lower premium.

Assuming flood is part of homeowners insurance? Read the flood section before you close.

Already have mortgage approval? Check how insurance costs and deductible choices fit your full monthly budget, and review the NAIC Consumer’s Guide to Home Insurance.

What Is a Homeowners Insurance Deductible?

A homeowners insurance deductible is the amount you must pay yourself on a covered claim before the insurer starts paying the rest, up to policy limits, as described by Citizens Property Insurance Corporation.

A deductible is not the same thing as a premium.

Premium: what you pay to keep the policy active

Deductible: what you pay after a covered loss happens

In plain language, a deductible is the portion of the loss you keep.

For example, if a covered non-hurricane claim causes $12,000 in damage and your all-other-perils deductible is $2,500, you would generally pay the first $2,500 and the insurer would pay the covered amount above that, subject to policy terms and limits.

That basic idea is simple. Florida gets more complicated because many policies also include a separate hurricane deductible.

Key takeaway: A deductible is a risk-sharing feature of the policy. A higher deductible usually means you agree to absorb more loss yourself in exchange for a lower premium, a tradeoff also explained by Bankrate and NerdWallet.

How Is a Florida Hurricane Deductible Different?

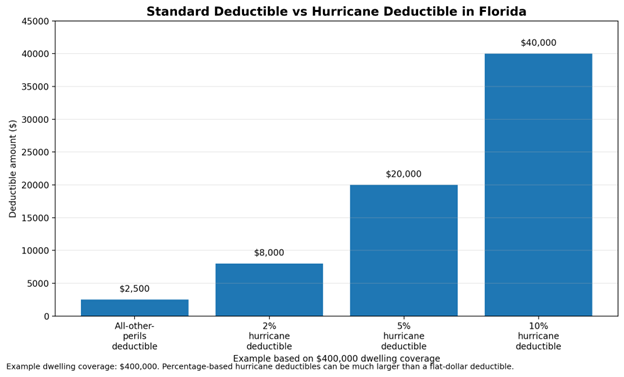

A Florida hurricane deductible is a separate deductible that applies to covered hurricane losses. It is often larger than a standard deductible and is commonly expressed as a percentage of the home’s insured dwelling limit rather than a flat dollar amount, according to the Florida Department of Financial Services.

Florida’s consumer guidance says insurers generally must offer hurricane deductible options of:

- $500

- 2% of dwelling or structure limits

- 5% of dwelling or structure limits

- 10% of dwelling or structure limits

The insurer must also prominently show the actual dollar value of the hurricane deductible on the declarations page or renewal materials, as required by Florida Statutes, Section 627.701.

That means a 2% hurricane deductible on a home insured for $400,000 is not $2,000. It is $8,000.

That is why deductible choice is not just a quote-shopping detail. It is a savings decision.

Key takeaway: A percentage-based hurricane deductible can create a much bigger out-of-pocket cost than buyers expect if they only look at the premium.

When Does the Hurricane Deductible Apply in Florida?

When Does the Hurricane Deductible Apply in Florida?

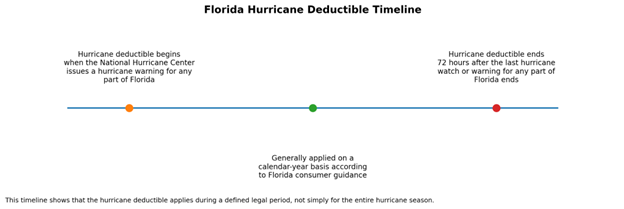

In Florida, the hurricane deductible applies only during the legally defined hurricane deductible period.

That period begins when the National Hurricane Center issues a hurricane warning for any part of Florida. It ends 72 hours after the last hurricane watch or hurricane warning for any part of Florida ends, under Florida Statutes, Section 627.4025.

Florida’s consumer guidance also highlights two practical rules that many homeowners do not know:

- When the hurricane deductible applies, no other deductible under the policy may also be applied to that same loss.

- The hurricane deductible is generally applied on a calendar-year basis, so once it has been satisfied for covered hurricane losses under the policy terms, it generally is not fully recharged again for each separate hurricane claim in that year.

This is also explained by the Florida Department of Financial Services and in the Citizens Property Insurance hurricane coverage guide.

That matters for budgeting. Your all-other-perils deductible may be $1,000 or $2,500, but your true storm exposure could be much higher.

Key takeaway: Your real storm deductible may be many times larger than your regular claim deductible.

Florida Hurricane Deductible Timeline

What Deductible Options Do Florida Homeowners Usually Have?

Florida homeowners often have a flat-dollar deductible for most covered losses and a separate hurricane deductible for hurricane losses.

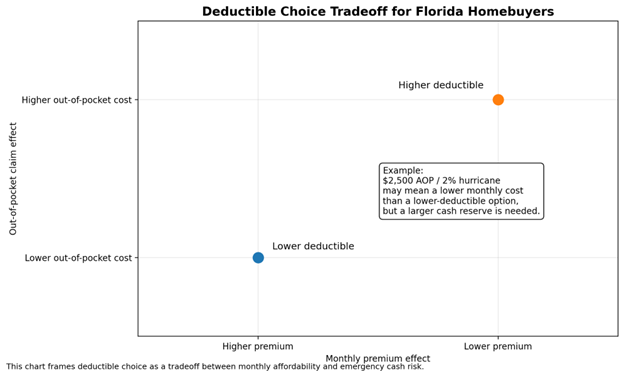

The real choice is not just “low” or “high.” It is whether the deductible matches your savings, risk tolerance, and storm exposure.

| Feature | Lower Deductible | Higher Deductible |

| Monthly premium | Usually higher | Usually lower |

| Out-of-pocket cost after a claim | Usually lower | Usually higher |

| Cash reserve needed | Smaller | Larger |

| Best fit | Buyers with limited emergency savings | Buyers with stronger cash reserves |

| Main risk | Higher ongoing cost | Bigger financial shock after a loss |

That tradeoff is common across homeowners insurance. Raising the deductible may lower the premium, but only if the homeowner can comfortably absorb the extra cost after a claim, as noted by Bankrate and NerdWallet.

Key takeaway: A lower premium is not always the better financial choice if the deductible would be painful to pay after a loss.

How Should Homebuyers Choose a Deductible?

The best deductible is usually the one you can afford without borrowing, missing mortgage payments, or delaying urgent repairs.

In Florida, that means evaluating both your standard deductible and your hurricane deductible, not just the premium on the quote.

A practical way to decide:

- Start with your emergency fund.

- Check the all-other-perils deductible.

- Check the hurricane deductible as a dollar amount, not just as a percentage.

- Ask whether you could pay that amount within days of a major loss.

- Compare the premium savings against the extra out-of-pocket risk.

- Review whether mitigation features or discounts could lower premium without forcing a higher deductible.

Florida encourages certain mitigation-related savings, and you can review the Florida DFS guide to premium discounts for hurricane loss mitigation and the broader Florida homeowners insurance guidance page.

The declarations page matters here. Florida requires the actual dollar amount of the hurricane deductible to be shown prominently so homeowners can understand the real exposure, under Florida Statutes, Section 627.701.

For a mortgage borrower, that is especially important because the lender may require insurance, but the lender is not the one paying the deductible after a storm.

Key takeaway: The right deductible should match your cash reserves, not just your wish for a lower premium.

What Does This Mean for Your Mortgage Budget?

A deductible is not part of your regular mortgage payment, but it is part of your real housing risk.

A lower premium from a higher deductible may help monthly affordability. But a higher deductible may leave you exposed to a major cash need after a claim.

From a mortgage-planning perspective, think in two buckets:

- Monthly housing cost: principal, interest, taxes, insurance, and possibly HOA dues

- Emergency housing cash: deductible, temporary repairs, and costs that are not reimbursed right away

That is why the cheapest insurance quote is not always the safest choice. A policy with a very high hurricane deductible may look manageable in the monthly budget but become painful after a real storm.

Key takeaway: Premium and deductible should be evaluated together, not separately.

Does Homeowners Insurance Cover Flood Damage in Florida?

Does Homeowners Insurance Cover Flood Damage in Florida?

Usually no.

Standard homeowners insurance generally does not cover flood damage. Flood insurance is usually separate and may be purchased through the National Flood Insurance Program via FEMA or a private insurer.

This is one of the most important points for Florida buyers.

Wind and rain damage from a covered peril may be handled one way under homeowners insurance. Rising water from outside the home is a different issue. Both FEMA and the NAIC flood insurance resource explain that standard homeowners insurance usually does not cover flood losses.

If flood risk is part of your property search, ask about flood coverage separately. A buyer who only understands the deductible on the homeowners policy may still have a major coverage gap.

Key takeaway: Do not assume your homeowners insurance deductible tells you anything about flood coverage unless you have a separate flood policy or endorsement that addresses it.

A Simple Roadmap for Choosing a Deductible in Florida

Choose your deductible by matching the policy to your savings, your property’s storm exposure, and your tolerance for financial shock after a claim.

Use this sequence:

- Ask for quotes with at least two deductible options

- Convert every percentage hurricane deductible into a dollar figure

- Decide what amount you could pay without taking on debt

- Review the declarations page before binding coverage

- Ask whether wind-mitigation discounts are available

- Confirm whether flood insurance is also needed

- Recheck your emergency fund after closing

Common Mistakes Florida Homebuyers Make

Common Mistakes Florida Homebuyers Make

Most deductible mistakes happen because buyers focus on premium and ignore claim-time cash needs.

Common examples include:

- Looking only at premium

- Ignoring the hurricane deductible

- Not reading the declarations page

- Assuming flood is covered

- Choosing a deductible larger than available savings

- Skipping mitigation conversations

- Not learning the claims process and claim-rights basics

In Florida, the most expensive version of this mistake is simple: a buyer chooses a lower monthly premium without realizing the hurricane deductible could mean several thousand dollars out of pocket after a storm.

Key takeaway: The biggest deductible mistakes usually happen before the first claim ever occurs.

Why Professional Help Matters

Insurance quotes can look simple when you compare them line by line, but the real risk often sits in the details:

- Hurricane deductible percentage

- Actual dollar amount on the declarations page

- Flood gap

- Wind-mitigation discounts

- What you could really afford after a claim

A mortgage professional can help you pressure-test how the insurance structure fits into your overall homebuying budget.

At Pegasus, the goal is not just to get you approved. It is to help you understand whether the full cost of owning the home still works when insurance risk is added honestly.

Example Scenario

A buyer compared two homeowners insurance quotes and chose the cheaper one at first glance. But once the hurricane deductible was converted into dollars, the lower-premium policy created much higher storm exposure. The better choice was not simply the cheapest quote. It was the one that fit the buyer’s emergency savings more realistically.

FAQ

What is a good homeowners insurance deductible in Florida?

A good deductible is one you can afford from savings without serious financial strain. In Florida, that means reviewing both the standard deductible and the hurricane deductible in dollar terms, as outlined by the Florida Department of Financial Services.

Is a hurricane deductible separate from a regular deductible?

Often yes. A Florida homeowners policy may include a separate hurricane deductible for covered hurricane losses and an all-other-perils deductible for many non-hurricane claims, as explained by the Florida Department of Financial Services.

When does the Florida hurricane deductible start and end?

It begins when the National Hurricane Center issues a hurricane warning for any part of Florida and ends 72 hours after the last hurricane watch or warning for any part of Florida ends, under Florida Statutes, Section 627.4025.

Does a higher deductible lower homeowners insurance premiums?

Often yes. A higher deductible may reduce your premium because you are agreeing to absorb more of the loss yourself. But the lower premium may not be worth it if you cannot afford the deductible after a claim, as explained by Bankrate and NerdWallet.

Are Florida insurers required to show the hurricane deductible in dollars?

Yes. Florida law requires the actual dollar value of the hurricane deductible to be displayed prominently on the declarations page or renewal materials for personal lines residential property insurance, under Florida Statutes, Section 627.701.

Can I be charged both my hurricane deductible and another deductible on the same hurricane loss?

No. Florida consumer guidance states that when the hurricane deductible is applied, no other deductible under the policy may also be applied to that same loss, according to the Florida Department of Financial Services.

Does homeowners insurance in Florida cover flooding?

Usually no. Flood damage is typically not covered by standard homeowners insurance and usually requires separate flood insurance, according to FEMA and the NAIC flood insurance resource.

Does my mortgage lender care which deductible I choose?

Your lender mainly cares that the property remains properly insured, but the deductible still matters because you are the one responsible for paying it after a covered loss. The NAIC homeowners insurance overview is helpful background on how coverage and lender expectations fit together.

Final Takeaway

A homeowners insurance deductible is not just an insurance detail. In Florida, it is a core homeownership budget decision.

The right deductible usually balances two goals:

- Keeping premiums manageable

- Keeping claim-time costs realistic

For many Florida buyers, the biggest mistake is comparing quotes without converting the hurricane deductible into a dollar amount and asking whether that amount could actually be paid from savings.

Before you close:

- Review the declarations page

- Ask about hurricane and flood exposure

- Confirm the real dollar deductible

- Make sure the choice fits both your monthly budget and your emergency savings

If you want help evaluating how insurance costs fit into your full mortgage budget, speak with a Pegasus mortgage professional before you finalize your home purchase.

Sources & References

- Florida Department of Financial Services, “Florida’s Hurricane Deductible”

https://myfloridacfo.com/division/consumers/consumerprotections/floridashurricanedeductible - Florida Department of Financial Services, “Homeowners Insurance | Full Coverage”

https://myfloridacfo.com/division/ica/fullcoverage/homeowners - Florida Statutes, Section 627.701

https://www.leg.state.fl.us/statutes/index.cfm?App_mode=Display_Statute&URL=0600-0699%2F0627%2FSections%2F0627.701.html - Florida Statutes, Section 627.4025

https://www.flsenate.gov/Laws/Statutes/2025/627.4025 - Florida Statutes, Section 627.7142, Homeowner Claims Bill of Rights

https://www.flsenate.gov/Laws/Statutes/2021/627.7142 - Citizens Property Insurance Corporation, “Deductibles”

https://www.citizensfla.com/deductibles - Citizens Property Insurance Corporation, “Hurricane Coverage: What You Need To Know”

https://www.citizensfla.com/documents/20702/31365/Hurricane%2BCoverage.pdf/ca95aa07-7ed9-4406-b431-3cd38b652848 - National Association of Insurance Commissioners, “Homeowners Insurance”

https://content.naic.org/insurance-topics/homeowners-insurance - National Association of Insurance Commissioners, “A Consumer’s Guide to Home Insurance”

https://content.naic.org/sites/default/files/publication-hoi-pp-consumer-homeowners.pdf - National Association of Insurance Commissioners, “Flood Insurance”

https://content.naic.org/consumer/flood-insurance.htm - FEMA, “Flood Insurance”

https://www.fema.gov/flood-insurance - Bankrate, “What Is a Homeowners Insurance Deductible?”

https://www.bankrate.com/insurance/homeowners-insurance/home-insurance-deductible/ - NerdWallet, “What Is a Homeowners Insurance Deductible?”

https://www.nerdwallet.com/insurance/homeowners/learn/homeowners-insurance-deductible