If you are buying in Florida right now, seller concessions may be one of the cleanest ways to make a deal work without draining your savings.

Many buyers are less worried about the sticker price alone and more worried about cash to close. Down payment, title charges, prepaid taxes and insurance, escrows, and lender fees can all hit at once. The Consumer Financial Protection Bureau says closing costs typically run about 2% to 5% of the home purchase price, not including the down payment.

That is why seller concessions matter in 2026. They can reduce upfront cash pressure, and in some cases they can help fund a temporary rate buydown. This guide explains how they work in Florida, how the rules change by loan type, when they make the most sense, and what buyers should check on the Loan Estimate and Closing Disclosure before they sign.

Quick Answer

Seller concessions can help Florida buyers reduce out-of-pocket closing costs and, in some cases, help fund a temporary rate buydown. They usually cannot replace your down payment, and the allowed amount depends on the loan program and sometimes your loan-to-value ratio. In Florida’s more balanced 2026 market, this strategy matters more because buyers still face meaningful cash-to-close pressure while inventory has improved enough in some areas to support more negotiation.

Key takeaway: The smart move is to match the concession request to your loan rules, your real closing costs, and your negotiating leverage in the local market.

What are seller concessions in Florida?

A seller concession is money from a party tied to the transaction, usually the seller, builder, or agent, that covers costs the buyer would otherwise pay at closing.

For conventional loans, Fannie Mae calls these interested party contributions, or IPCs. Fannie says IPCs are contributions from third parties with a vested interest in the transaction and that they are used to cover costs that are typically the buyer’s responsibility.

Just as important, Fannie also says those funds cannot be used to:

- make the borrower’s down payment

- meet reserve requirements

- satisfy the minimum borrower contribution requirement

That is the core rule buyers need to understand before asking for “seller-paid closing costs.”

A seller concession is not free money. The CFPB explains that while buyers can negotiate a seller credit toward closing costs, the seller will often want a higher price to cover that credit. So the real question is not just whether you can get a concession. It is whether a concession helps your situation more than a price cut would.

A clean definition to remember: a seller concession is a negotiated credit that shifts eligible closing costs from the buyer to the seller, subject to program limits and full disclosure at closing.

How much can a seller contribute under different loan types?

How much can a seller contribute under different loan types?

The cap depends on the loan program.

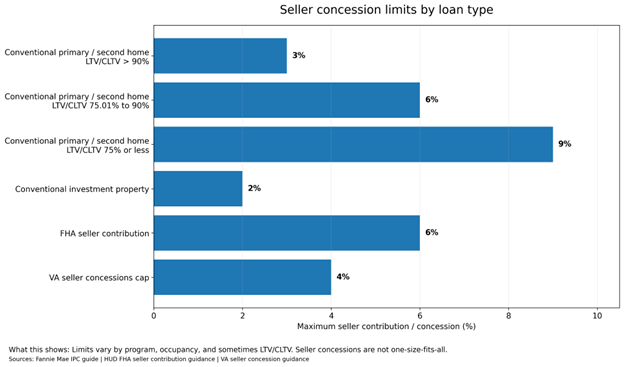

For conventional loans sold to Fannie Mae, the current limits are clear. Fannie’s IPC guide says that for a principal residence or second home, the maximum financing concession is:

- 3% when the LTV or CLTV is greater than 90%

- 6% when the LTV or CLTV is 75.01% to 90%

- 9% when the LTV or CLTV is 75% or less

For investment properties, the cap is 2% across all CLTV ratios.

Fannie also says that financing concessions above those limits become sales concessions, which means they must be deducted from the property’s sales price for underwriting purposes.

For FHA, official HUD guidance says sellers or other interested parties can contribute up to 6% of the property’s sale price toward the buyer’s actual allowable closing costs, prepaid expenses, discount points, and other permitted costs.

For VA loans, the structure is different. The Department of Veterans Affairs says on its temporary buydown page that temporary buydowns funded by the seller or builder count as a seller concession, and seller concessions are capped at 4% of the reasonable value.

Here is the practical snapshot:

| Loan type | Typical concession rule | What buyers should remember |

| Conventional (Fannie Mae) | 3%, 6%, or 9% for primary or second homes depending on LTV; 2% for investment property | Excess can become a sales concession and affect underwriting |

| FHA | Up to 6% of sale price toward allowable costs | Often helpful when cash to close is tight |

| VA | Seller concessions capped at 4% of reasonable value; seller-funded temporary buydowns count toward that cap | Buyer must still qualify at the full payment |

Decision checkpoint: Before you ask for a number, know your loan program, occupancy type, and how much room your file actually has under the cap.

Can seller concessions cover a rate buydown?

Yes, sometimes.

For conventional loans, Fannie says in its IPC rule that if a temporary or permanent interest rate buydown is funded by an interested party, the cost of that subsidy must be included in the IPC calculation.

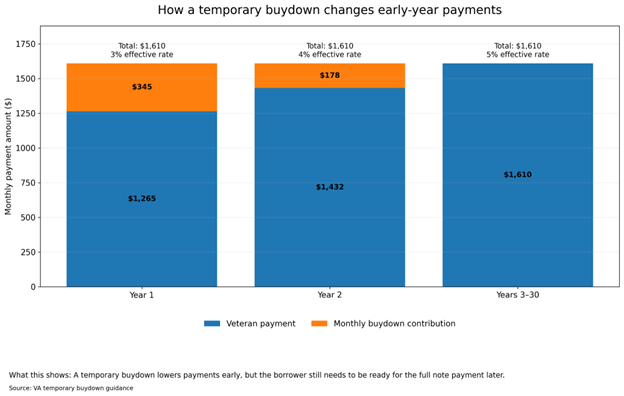

For VA, the rule is explicit. The VA says on its temporary buydown guidance that seller- or builder-funded temporary buydowns are considered seller concessions and count toward the program cap.

But there is a limit buyers should not miss: the VA also says lenders must base qualification on the full monthly payment after the temporary buydown ends. In other words, a buydown can improve early-year payment relief, but it cannot be used to qualify a borrower for a payment they will not be able to afford later.

That is why the right comparison is usually this:

- Seller-paid closing costs help most when cash to close is the biggest problem.

- A temporary buydown helps most when monthly payment pressure is the bigger concern in the first year or two.

- A price cut may help long-term borrowing cost more than a credit does, depending on the size of the adjustment.

If your real pain point is monthly payment, ask your lender to compare the concession-as-credit option against the concession-as-buydown option before you write the offer.

When do seller concessions make the most sense in Florida’s 2026 market?

This strategy usually makes the most sense when cash to close is your main obstacle, when the property has been sitting longer, or when the seller wants to preserve the headline price.

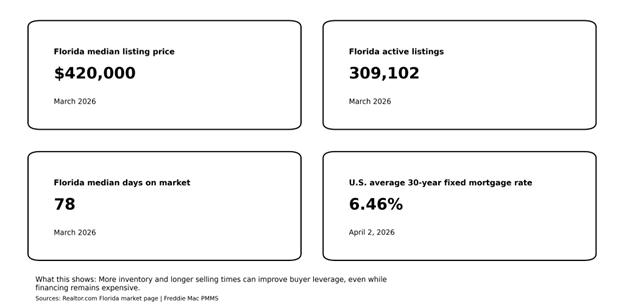

Florida is not behaving like the ultra-tight market many buyers remember. Realtor.com’s Florida market snapshot shows that as of March 2026, the state had a $420,000 median listing price, 309,102 active listings, and 78 median days on market.

Florida Realtors also said in its January 2026 state market outlook that Florida’s housing market was entering a “more balanced and opportunity-rich phase.”

That does not mean every Florida city is easy for buyers. But it does mean there are more situations where sellers care about net proceeds, timing, and deal certainty just as much as price.

Borrowing costs are still meaningful too. Freddie Mac’s Primary Mortgage Market Survey showed the average 30-year fixed-rate mortgage at 6.46% as of April 2, 2026.

In that kind of rate environment, concessions can be especially useful on:

- listings with longer days on market

- resales where the seller wants to avoid another price cut

- builder inventory homes

- deals where the seller wants to keep neighborhood comparable sales stronger

- transactions where cash to close feels heavier because of escrows, taxes, insurance, or condo-related costs

Bottom line: In a more balanced market, seller concessions can solve a real affordability problem without forcing a large visible price cut.

Why Florida buyers have more room to negotiate in 2026

Is a seller concession better than a price cut?

It depends on which problem you are actually trying to solve.

If your biggest problem is cash to close, a concession is often more useful than a modest price reduction. The CFPB’s homebuying budgeting guidance makes clear that closing costs can be significant. Reducing those costs directly can help more than trimming the price a little.

If your biggest problem is long-term payment cost, a price cut may help more than a closing-cost credit. That is because lowering the loan amount can reduce the payment for the full life of the loan, not just at closing.

If your biggest problem is short-term payment relief, a temporary buydown may be the better use of the available seller money, assuming your program allows it and your lender confirms the numbers.

There is also one important limit. Fannie says any financing concession that exceeds the borrower’s closing costs must be treated as a sales concession. In plain English, that means the excess does not turn into cash back in your pocket.

The best concession is not the biggest one. It is the one that matches your actual numbers.

How should Florida buyers negotiate seller concessions?

The best negotiation starts with math, not hope.

A practical roadmap looks like this:

- Know your loan program first. Conventional, FHA, and VA do not use the same framework.

- Estimate your real closing costs. Use lender numbers, not internet averages alone.

- Decide what kind of help you need. Cash-to-close relief, monthly payment relief, and price relief are not the same thing.

- Match the request to the property. Credits are usually easier to justify on stale listings, builder inventory, or properties facing more competition.

- Keep the file clean. Fannie warns that mortgages with undisclosed IPCs are not eligible for sale.

This is also where your paperwork matters.

The CFPB says a Loan Estimate must be provided within three business days of receiving your application, and its Loan Estimate explainer tells buyers to confirm the estimated cash to close and whether seller credits are reflected correctly.

Later in the process, the CFPB says lenders must provide the Closing Disclosure three business days before scheduled closing. Use that review window to confirm that the seller credit matches what was negotiated.

What should buyers check on the Loan Estimate and Closing Disclosure?

These two forms are where a good negotiation either shows up correctly or starts to go wrong.

On the Loan Estimate, buyers should check:

- that the loan amount matches the structure they expected

- that the estimated cash to close reflects the planned seller credit

- whether there are lender credits, points, or other trade-offs affecting the rate

- whether taxes, insurance, and escrow estimates look realistic

The CFPB’s interactive Loan Estimate guide specifically tells buyers to review the estimated closing costs, the estimated cash to close, and whether seller credits are reducing the amount they need to bring.

On the Closing Disclosure, buyers should check:

- that the seller credit reflects what was agreed with the seller

- that cash to close matches expectations

- that any “Seller Paid” line items are accurate

- that the final interest rate, payment, and total closing costs match the deal they accepted

The CFPB’s Closing Disclosure explainer specifically highlights the seller credit section and tells buyers to use the three-day review period to resolve differences before closing.

Common mistakes buyers make with seller concessions

Most mistakes happen when buyers focus only on the contract price and ignore the loan mechanics.

Common errors include:

- asking for a credit before checking the program cap

- trying to use the credit for the down payment

- asking for more than actual eligible closing costs

- ignoring appraisal risk if the price is pushed up to support the credit

- choosing a credit when a price cut would help more

- failing to confirm the credit on the final paperwork

- overlooking that builder- or seller-funded buydowns still count under the relevant cap

If X is true, consider Y: if your problem is cash to close, negotiate the credit first. If your problem is monthly payment, compare a buydown with a price cut before you decide.

Frequently asked questions

Frequently asked questions

Can seller concessions cover my down payment?

Usually no. For conventional loans, Fannie Mae’s IPC rule says interested party contributions can cover eligible closing costs, but they cannot be used for the borrower’s down payment, reserve requirements, or minimum borrower contribution.

How much can a seller contribute toward closing costs?

It depends on the loan type. On conventional loans sold to Fannie Mae, the cap varies by occupancy and loan-to-value ratio. FHA allows interested parties to contribute up to 6% of the sale price toward allowable costs under HUD guidance. VA uses a different structure, including a 4% seller-concession cap in the contexts described on the VA temporary buydown page.

Can seller concessions pay for a rate buydown?

Yes, sometimes. For conventional loans, Fannie Mae says interested-party-funded temporary or permanent buydowns must be counted inside the IPC calculation. For VA loans, the VA says seller- or builder-funded temporary buydowns count as seller concessions and still must fit inside the program limits.

Are seller concessions easier to negotiate in Florida right now?

In some parts of Florida, yes. With more inventory and longer days on market than during the tightest years of the market, some sellers may be more open to credits than they were before. That does not mean every submarket is soft, but it does mean buyers may have more room to negotiate when a listing has lingered or a seller wants a cleaner deal.

Can seller concessions lower cash to close without lowering the home price?

Yes. That is one of the main reasons buyers use them. A seller credit can reduce the amount of cash you need to bring to closing even when the contract price stays the same. The trade-off is that the seller may want to keep the price higher in exchange for the credit, so the better comparison is always the net result, not just the headline number.

What should I check on the Loan Estimate and Closing Disclosure?

On the Loan Estimate, check estimated cash to close, seller credits, points, lender credits, and whether the loan structure matches what you discussed. On the Closing Disclosure, confirm the seller credit appears correctly, the final cash to close is accurate, and the rate and payment match the deal you agreed to.

Do seller concessions hurt loan approval?

Not by themselves. The issue is whether the concession is structured inside the program rules, fully disclosed, and supported by the appraisal and underwriting file. Problems usually come from asking for too much, using the wrong structure for the loan type, or failing to document the credit correctly.

Is a seller concession better than a price cut?

It depends on your problem. If you are short on liquid cash, a concession may help more. If your bigger concern is long-term payment cost, a price cut may help more. If your concern is early-year payment relief, a temporary buydown may be worth comparing. The smartest move is to have your lender model all three before you decide.

Why professional help matters here

On paper, seller concessions sound simple. In practice, they sit at the intersection of contract strategy, underwriting rules, appraisal risk, and closing disclosure accuracy.

A generic calculator will not tell you:

- whether your file has room under the loan-program cap

- whether a buydown would help more than a closing-cost credit

- whether your seller credit is large enough to matter but small enough to stay clean

- whether the final numbers on the disclosure forms match the structure you negotiated

That is where a mortgage professional can add real value. A good review should compare a seller credit, a price cut, and a buydown side by side so you can see which one actually improves your deal.

What Florida buyers should remember before making the offer

Before you write the offer, keep these three points in mind:

- Seller concessions are a negotiation tool, not free money.

- They work best when they solve a specific problem, like cash-to-close pressure or early-year payment strain.

- They only help if they fit your loan rules and are documented correctly from contract to closing.

Stop guessing. Before you negotiate, ask your lender to model three versions of the same offer: one with a seller credit, one with a price cut, and one with a buydown if your program allows it. That comparison will usually show which option helps your budget most without creating underwriting problems.

If you want help comparing those scenarios on a Florida purchase, speak with a Pegasus mortgage professional before you submit the offer.

Disclaimer: This article is general information, not legal or lending advice. Seller concessions depend on loan type, occupancy, appraised value, underwriting, and the actual costs on your transaction. Rules can also differ between conventional, FHA, VA, and lender overlays, so buyers should confirm the final structure with their mortgage professional before making an offer.

Sources & References

- Fannie Mae — Interested Party Contributions (IPCs)

https://selling-guide.fanniemae.com/sel/b3-4.1-02/interested-party-contributions-ipcs - VA Home Loans — Temporary Buydowns

https://www.benefits.va.gov/homeloans/temporary-buydown.asp - VA Home Loans — Loan Fees / Seller Concessions

https://www.benefits.va.gov/HOMELOANS/purchaseco_loan_fee.asp - HUD / FHA — Seller or Interested-Party Contributions (official archived page)

https://archives.hud.gov/offices/hsg/sfh/ref/sfhp2-18.cfm - CFPB — Figure out how much you want to spend

https://www.consumerfinance.gov/owning-a-home/prepare/figure-out-how-much-you-want-to-spend/ - CFPB — What fees or charges are paid when closing and who pays them?

https://www.consumerfinance.gov/ask-cfpb/what-fees-or-charges-are-paid-when-closing-on-a-mortgage-and-who-pays-them-en-1845/ - CFPB — Loan Estimate Explainer

https://www.consumerfinance.gov/owning-a-home/loan-estimate/ - CFPB — What is a Loan Estimate?

https://www.consumerfinance.gov/ask-cfpb/what-is-a-loan-estimate-en-1995/ - CFPB — What documents should I receive before closing on a mortgage loan?

https://www.consumerfinance.gov/ask-cfpb/what-documents-should-i-receive-before-closing-on-a-mortgage-loan-en-181/ - CFPB — Closing Disclosure Explainer

https://www.consumerfinance.gov/owning-a-home/closing-disclosure/ - CFPB — What is a Closing Disclosure?

https://www.consumerfinance.gov/ask-cfpb/what-is-a-closing-disclosure-en-1983/ - Freddie Mac — Primary Mortgage Market Survey (PMMS)

https://www.freddiemac.com/pmms - Realtor.com — Florida Housing & Rental Market Trends

https://www.realtor.com/local/market/florida - Florida Realtors — 2026 Real Estate Trends: Fla. Housing Market Stabilizing as Buyer Demand Builds

https://www.floridarealtors.org/newsroom/2026-real-estate-trends-fla-housing-market-stabilizing-buyer-demand-builds - Florida Realtors — A More Balanced Housing Market Emerging

https://www.floridarealtors.org/news-media/news-articles/2026/03/more-balanced-housing-market-emerging