Buying a home should feel exciting. But for many buyers, the final stretch is where identity theft protection matters most.

That is because homebuyers are moving fast, sharing sensitive documents, wiring large sums, and expecting urgent messages from lenders, title companies, attorneys, and real estate professionals. One fake email that looks almost right can arrive at exactly the wrong time. One routine-looking request can become a stolen down payment or a painful credit-repair process.

In 2026, identity theft protection is an essential part of buying a home in Florida. This guide explains the biggest threats buyers should watch for, how real estate wire fraud works, what information you should never send casually, and what steps can help protect your identity, money, and credit before closing day.

For related guidance, see our mortgage document checklist for Florida buyers, what happens at closing in Florida, and first-time homebuyer mistakes to avoid in Florida.

What identity theft protection risks matter most to Florida homebuyers?

The biggest risks identity theft protection should address are usually:

- real estate wire fraud

- email impersonation

- stolen personal documents

- account takeover

- misuse of identity data collected during mortgage underwriting

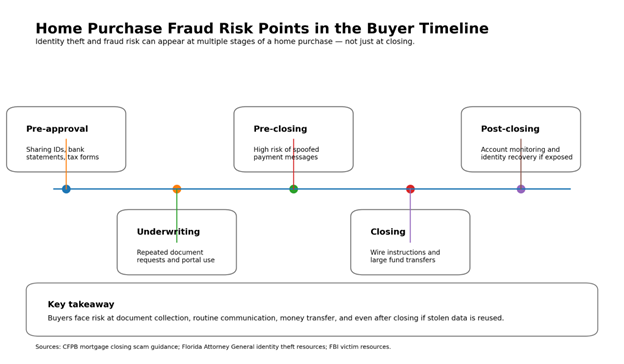

These risks matter because homebuyers often share bank statements, tax forms, government ID, payroll records, and payment instructions during a short, high-pressure timeline.

Florida’s Attorney General describes identity theft broadly and explains that a wide range of personal information can be misused, including a person’s name, address, date of birth, Social Security number, driver license number, and financial account information, as outlined in the state’s identity theft consumer resource guide.

Real estate wire fraud is one of the most urgent risks in a purchase. The Consumer Financial Protection Bureau warns that scammers target homebuyers during the closing process and may pose as a trusted person involved in the deal.

For buyers, identity theft protection is not just about preventing someone from opening a credit card in your name. It also means reducing the chance that criminals can use stolen details to redirect funds, break into your email, fake authorizations, or manipulate closing communications.

Key takeaway: A home purchase creates exactly the kind of high-trust, high-dollar environment scammers look for, which is why identity theft protection should be part of the process from day one.

How does wire fraud affect identity theft protection during a home purchase?

How does wire fraud affect identity theft protection during a home purchase?

Wire fraud usually happens when a buyer receives payment instructions that look legitimate but are actually fake.

The criminal often relies on three things:

- timing, because buyers expect urgent money instructions right before closing

- realism, because the email or message may closely resemble a legitimate professional

- pressure, because the buyer is told to act quickly and not slow the process down

The CFPB’s mortgage closing scam warning recommends identifying trusted people in advance and confirming payment instructions outside email before sending funds.

The broader fraud environment is also getting more expensive. The FBI’s April 2025 release on the 2024 IC3 report says internet crime complaints in 2024 detailed reported losses exceeding $16 billion, and Florida was among the states with the most complaints.

Watch for these red flags:

- a last-minute change to wiring instructions

- a message telling you the matter is urgent

- small spelling changes in an email address or domain

- a request to send money to a new account

- pressure to avoid calling anyone for confirmation

- payment instructions sent only by email, with no prior verbal verification

Decision checkpoint: If payment instructions change late in the deal, stop and verify by phone using a number you already trust.

What should homebuyers never do with personal information?

Homebuyers should not treat sensitive identity and banking details like routine paperwork.

As a rule, strong identity theft protection means avoiding these habits:

- sending Social Security numbers or bank details through ordinary email when a secure portal is available

- clicking links in unexpected document requests

- reusing weak passwords across email and banking

- using public Wi-Fi for document upload or account access

- replying directly to a suspicious message instead of calling a trusted number on file

The FBI’s identity theft victim resources explain that stolen personal information may be used to access bank accounts, complete wire transactions, and open fraudulent bank or credit accounts. That is especially relevant in mortgage underwriting, where buyers may be asked for exactly the records criminals want.

If a secure portal exists, use it. If a request feels unusual, verify it before you upload or send anything.

Which identity theft protection tools should buyers consider?

Which identity theft protection tools should buyers consider?

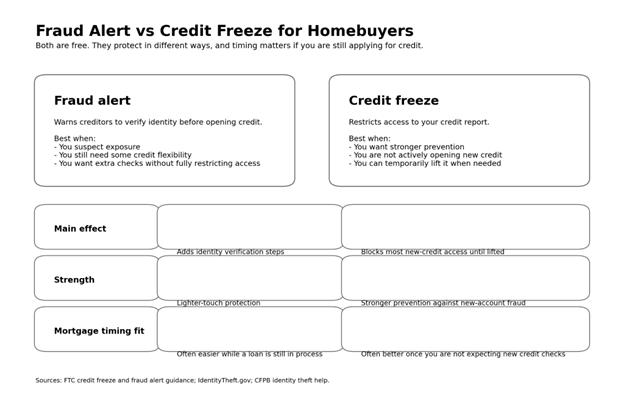

A fraud alert and a credit freeze are both free tools, but they do different jobs.

A credit freeze makes it much harder for anyone to open a new credit account in your name. The FTC explains that freezes are free, do not affect your credit score, and stay in place until you lift them.

A fraud alert tells lenders to take extra steps to verify your identity before issuing new credit. The FTC says an initial fraud alert is also free and generally lasts one year.

Here is the practical comparison:

- Fraud alert: Better when you suspect risk or exposure but still need some credit flexibility during underwriting.

- Credit freeze: Stronger when you want tighter identity theft protection against new-account fraud, especially after closing or anytime you are not actively applying for credit.

- Fraud alert: Credit can still be granted after extra checks.

- Credit freeze: New credit is harder to open unless you temporarily lift the freeze.

The CFPB’s identity theft guidance also notes that if your identity is stolen, you can place a fraud alert or security freeze with the credit reporting companies.

If you are still applying for a mortgage, timing matters. A freeze can protect you, but it can also interrupt a legitimate credit pull until you lift it.

Are Florida buyers especially exposed?

Florida buyers should take identity theft protection seriously, but the strongest support is for caution, not panic.

The FBI’s 2024 Internet Crime Report release says Florida was among the states with the most internet crime complaints in 2024. Florida’s Attorney General also maintains an identity theft resource center and a dedicated Identity Theft Victim Kit, which reflects the ongoing need for consumer guidance in the state.

That does not mean every Florida homebuyer is likely to be targeted. It does mean Florida buyers should use stricter verification habits whenever money or identity information is involved.

Bottom line: The risk is real enough that buyers should build identity theft protection checks into the process from day one.

Why professional help still matters

Generic safety advice is useful, but a real estate transaction creates timing issues that general identity theft protection advice does not always cover.

A mortgage professional, title company, or closing attorney should be able to tell you:

- how wiring instructions will be delivered

- who is allowed to send payment details

- which phone numbers you should use for confirmation

- when final funds are due and what changes would be unusual

That matters because the safest process is one that is agreed on before money moves.

A buyer who knows exactly how the closing team communicates is much harder to fool than a buyer improvising under pressure.

Step-by-step identity theft protection roadmap during the home-buying process

Step-by-step identity theft protection roadmap during the home-buying process

Before the transaction gets busy, ask your lender, title company, or attorney how instructions will be sent and how they want you to verify them.

Then follow this checklist:

- Identify two trusted contacts involved in the transaction and save their phone numbers from a known-good source.

- Use secure portals for documents whenever possible instead of ordinary email attachments.

- Turn on multi-factor authentication for email, banking, and cloud storage accounts.

- Treat any last-minute change in wiring instructions as suspicious until verified by phone.

- Review your credit and consider a fraud alert or freeze if your information was exposed.

- Keep records of every request, confirmation, and payment communication.

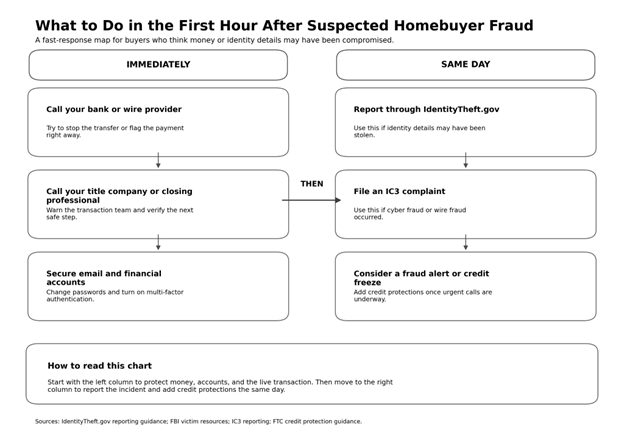

- If you already sent money to the wrong account, contact your bank and the closing professionals immediately.

- Report the incident to IC3 and start the identity theft recovery process at IdentityTheft.gov.

Florida’s Identity Theft Victim Kit also recommends quickly contacting the three major credit bureaus, your creditors, and your bank once misuse is discovered.

Common mistakes homebuyers make

- Trusting email too much

- Assuming urgency proves legitimacy

- Sending sensitive data through unsecured channels

- Using the phone number listed in the suspicious message

- Waiting too long after a suspected theft

- Ignoring free identity theft protection tools

- Reusing passwords across email and financial accounts

FAQ

What is the biggest identity theft protection risk for homebuyers?

For many buyers, the biggest immediate risk is real estate wire fraud tied to closing funds. The CFPB warns that scammers may impersonate trusted people in the transaction and send false wiring instructions.

Is wire fraud the same as identity theft?

Not exactly. Wire fraud focuses on stealing money through false payment instructions, while identity theft involves misuse of personal information to commit fraud. In real estate, the two often overlap.

Should I send wiring instructions by email?

Do not rely on email alone for wiring instructions. Use a trusted contact outside email to confirm payment details before sending money.

What if my Social Security number or bank details were exposed?

Move quickly. The CFPB says you can place a fraud alert or security freeze, and the federal IdentityTheft.gov portal offers step-by-step recovery help.

Are fraud alerts and credit freezes free?

Yes. The FTC says both are free. They work differently, so the better fit depends on whether you still need lenders to access your credit during the transaction.

What should I do if I sent money to a scammer?

Contact your bank and the professionals handling the closing immediately. The FBI says victims of internet crime should notify the financial institutions involved right away and submit a complaint through IC3.

Does Florida offer identity theft protection help for residents?

Yes. Florida’s Attorney General offers an identity theft resource center and an Identity Theft Victim Kit to help residents organize recovery steps.

Can a credit freeze interfere with a mortgage application?

It can. A credit freeze may block a lender from pulling your credit until you temporarily lift it.

The bottom line on identity theft protection during a home purchase

Identity theft protection in a Florida home purchase is not optional background advice. It is part of protecting your money, credit, and closing process.

The most important habit is simple: never treat a money request or identity request as routine just because it looks familiar. Verify first. Slow down. Use trusted channels. Protect your email and credit. And if something feels off, act immediately.

Stop guessing. Build an identity theft protection process before closing day. Bring your closing contacts, expected payment steps, and any suspicious message to a mortgage professional so you can confirm the safe next move before money or documents leave your hands.

Disclaimer: This article is general education, not legal, tax, cybersecurity, or financial advice. Fraud tactics change often, and your lender, title company, attorney, bank, and law enforcement contacts may give case-specific instructions. Always follow verified instructions from the professionals handling your transaction.

Sources & References

- FTC Consumer Sentinel Network Data Book 2024

https://www.ftc.gov/system/files/ftc_gov/pdf/csn-annual-data-book-2024.pdf - FTC press release on 2024 fraud losses

https://www.ftc.gov/news-events/news/press-releases/2025/03/new-ftc-data-show-big-jump-reported-losses-fraud-125-billion-2024 - CFPB mortgage closing scam warning

https://www.consumerfinance.gov/owning-a-home/beware-mortgage-closing-scams/ - CFPB identity theft recovery FAQ

https://www.consumerfinance.gov/ask-cfpb/what-do-i-do-if-i-think-i-have-been-a-victim-of-identity-theft-en-31/ - FTC credit freezes and fraud alerts

https://consumer.ftc.gov/articles/credit-freezes-and-fraud-alerts - IdentityTheft.gov reporting portal

https://www.identitytheft.gov/report/report - IdentityTheft.gov credit freeze guidance

https://www.identitytheft.gov/credit-freeze - FBI identity theft victim resources

https://www.fbi.gov/how-we-can-help-you/victim-services/seeking-victim-information/identity-theft-victim-resources - FBI / IC3 2024 Annual Report

https://www.ic3.gov/AnnualReport/Reports/2024_IC3Report.pdf - Florida Attorney General identity theft resource center

https://www.myfloridalegal.com/identity-theft/identity-theft - Florida Attorney General identity theft victim kit

https://www.myfloridalegal.com/identity-theft/identity-theft-victim-kit - Florida Department of Agriculture and Consumer Services security freeze FAQ

https://www.fdacs.gov/Consumer-Resources/Scams-and-Fraud/Identity-Theft/Identity-Theft/Security-Freeze-Credit-Report-FAQ