In 2026, Florida homebuyers should carefully research flood insurance options due to varying risk levels and coverage options. Flood insurance is required in high-risk flood zones (SFHA) and is recommended even in lower-risk areas. The National Flood Insurance Program (NFIP) offers federal coverage, but private flood insurance may provide better options for some buyers. Costs are influenced by location, property value, and coverage limits.

Flooding is a significant concern for homeowners in Florida, especially with the state’s exposure to hurricanes, tropical storms, and rising sea levels. If you’re considering buying a home in Florida, understanding flood insurance is crucial. Not only does it provide essential protection against flooding damage, but it can also help you navigate mandatory insurance requirements in flood-prone areas. However, many Florida buyers are confused about their flood insurance options, and it’s easy to feel overwhelmed by the choices and associated costs. This article will guide you through everything you need to know about flood insurance in Florida in 2026, helping you make an informed decision.

Quick Start: Pick Your Path

Choose your path to find the relevant section for your needs:

- First-Time Homebuyer: Explore flood insurance basics and coverage options.

- Current Homeowner: Learn about updating your flood insurance or switching providers.

- High-Risk Flood Zone Resident: Understand flood insurance requirements and costs for properties in Special Flood Hazard Areas (SFHA).

- Low/Moderate Risk Zone Resident: Assess whether flood insurance is worth it and understand optional coverage.

What is Flood Insurance and Why Is It Important for Florida Homebuyers?

Flood insurance is a policy that provides coverage for damage caused by flooding, which is typically excluded from standard home insurance policies. It’s essential for Florida homebuyers because the state is prone to hurricanes, floods, and storm surges, making flood risk a real concern.

In Florida, flood insurance is crucial for protecting your property against water damage that can occur from storms, hurricanes, or even heavy rains. Unlike regular homeowners insurance, which often excludes flooding, flood insurance specifically covers damages caused by floods. Florida’s location in a high-risk zone for flooding means that many homebuyers will be required to obtain flood insurance. Even those in lower-risk areas may consider purchasing additional coverage to mitigate the risk of flooding.

Do I Need Flood Insurance in Florida?

Flood insurance is mandatory for properties in high-risk flood zones (SFHA), but even if your home is in a moderate or low-risk area, purchasing flood insurance is highly recommended in Florida.

Florida’s flood zones are divided into high-risk areas (SFHA) and moderate/low-risk zones. Homes in SFHAs, particularly those located in coastal regions or near rivers, require flood insurance if they have a mortgage from a federally backed lender. For homes in moderate or low-risk zones, flood insurance is optional but still a smart choice due to Florida’s history of flooding from heavy rains and storms. If you live in a zone with a low chance of flooding, your premiums will be lower, but the protection can save you significantly in the event of an unexpected flood.

What Are the Costs of Flood Insurance in Florida?

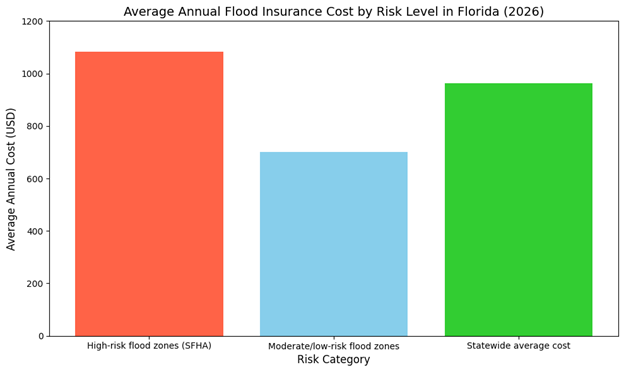

The cost of flood insurance in Florida varies depending on factors like location, risk zone, property value, and coverage limits. On average, homeowners can expect to pay between $700 and $1,200 annually for flood insurance.

Flood insurance premiums are primarily influenced by the flood zone in which your property is located. Homes in high-risk flood zones generally pay more for flood insurance due to the increased risk. On the other hand, homes in lower-risk zones may pay less. In 2026, the average annual cost for flood insurance in Florida is around $964, with costs ranging from $700 for properties in lower-risk areas to over $1,083 for homes in high-risk zones. It’s important to assess your flood risk and evaluate different policy options to find a plan that fits your budget and coverage needs.

What Coverage Options Are Available for Florida Homebuyers?

What Coverage Options Are Available for Florida Homebuyers?

Florida buyers can choose between federal flood insurance under the National Flood Insurance Program (NFIP) or private flood insurance, which may offer higher coverage limits and more flexible options.

There are two primary options for flood insurance in Florida: the National Flood Insurance Program (NFIP), which is federally backed, and private flood insurance policies offered by private insurance companies.

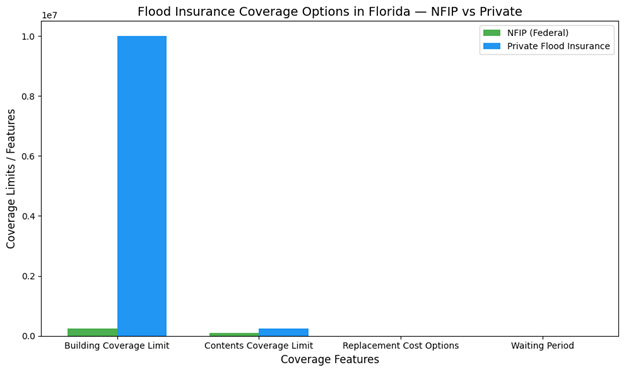

- NFIP provides standardized coverage limits: up to $250,000 for building coverage and up to $100,000 for contents.

- Private flood insurance offers more customizable policies with higher coverage limits and faster claim processing times, but it can be more expensive.

For many Florida homeowners, private insurance might offer better coverage for high-value homes or those in particularly high-risk flood areas. However, the NFIP remains the most common option, especially for those with federally backed mortgages.

How Do Flood Zones Affect My Home Insurance?

How Do Flood Zones Affect My Home Insurance?

Flood zones play a significant role in determining the cost and necessity of flood insurance. Homes in high-risk flood zones (SFHA) will face mandatory flood insurance requirements, while homes in low-risk zones may only need flood insurance for financial protection.

Flood zones are designated areas that indicate the likelihood of flooding, with high-risk zones (SFHAs) having a higher chance of experiencing floods. Homes located in SFHAs are required by law to carry flood insurance if they have a mortgage from a federally regulated lender. For properties in low to moderate-risk zones, flood insurance is not mandatory but is still a smart investment. Understanding your property’s flood zone is critical when shopping for flood insurance and determining the appropriate level of coverage.

Common Mistakes to Avoid When Purchasing Flood Insurance

Some common mistakes Florida homebuyers make when purchasing flood insurance include underestimating their flood risk, not understanding policy limits, and failing to review private flood insurance options.

Avoid these common errors when purchasing flood insurance:

- Underestimating risk: Many buyers assume they don’t need flood insurance because their property is in a moderate-risk area. This can be costly if a flood occurs unexpectedly.

- Ignoring policy limits: NFIP policies have coverage limits that may not fully cover your home’s value. Be sure to evaluate whether private insurance could offer higher limits.

- Not comparing providers: Private flood insurance may offer better options than the NFIP, especially for homes in high-risk zones. Always shop around to ensure you’re getting the best coverage for your needs.

Comparison Table: NFIP vs. Private Flood Insurance

| Feature | NFIP (Federal) | Private Flood Insurance |

| Building Coverage Limit | $250,000 | Up to $10,000,000+ |

| Contents Coverage Limit | $100,000 | $250,000+ |

| Replacement Cost Options | Limited | Often available |

| Waiting Period | 30 days | 10–15 days (varies) |

FAQ Section

What is the difference between home insurance and flood insurance in Florida?

Home insurance typically covers damages to your home from fire, theft, and other events, but it does not include flooding. Flood insurance specifically covers water damage caused by flooding events, including those from hurricanes and storms.

How much does flood insurance cost in Florida?

Flood insurance costs in Florida vary by location, risk zone, and coverage levels. On average, homeowners can expect to pay between $700 and $1,200 annually.

Do I need flood insurance if I live in a low-risk area?

While flood insurance is not mandatory in low-risk areas, it is still highly recommended. Florida’s unpredictable weather makes it prone to flooding, even in areas that are not in high-risk flood zones.

How long is the waiting period for flood insurance coverage to begin?

NFIP flood insurance policies typically have a 30-day waiting period before coverage begins. Private insurance may offer faster coverage, sometimes as soon as 10–15 days.

Can private flood insurance provide better coverage than NFIP?

Yes, private flood insurance often offers higher coverage limits, more flexible policy options, and faster claims processing compared to NFIP policies. It may be a better option for high-value homes or properties in high-risk flood zones.

Is flood insurance required for all Florida homebuyers?

Flood insurance is required for homes in high-risk flood zones (SFHA) with a federally backed mortgage. However, for homes in moderate to low-risk areas, flood insurance is not mandatory but is recommended.

Closing Section

Flood insurance is a vital part of protecting your home in Florida. Whether you’re in a high-risk flood zone or a more moderate area, securing the right flood insurance policy can save you from costly damage and long-term repair bills. If you’re unsure about your options, reach out to a Florida mortgage professional who can guide you through the process of finding the best flood insurance for your needs. Don’t wait until it’s too late—protect your home and peace of mind today.

Sources & References:

- FEMA — National Flood Insurance Program: fema.gov

- Florida Department of Financial Services — Flood Insurance FAQs: myfloridacfo.com

- Compare.com — Florida Flood Insurance Guide: compare.com

- Policygenius — Flood Insurance in Florida: policygenius.com