Last updated: April 2026

Disclaimer: This article is general information, not legal, tax, or personalized mortgage advice. Buydown availability, underwriting, seller-credit limits, and closing treatment vary by loan program, lender, investor, and contract terms.

A lot of Florida buyers in 2026 are not asking whether they want a house. They are asking whether they can survive the payment.

That is why 2-1 buydowns are back in the conversation. On paper, they look attractive: lower payments for the first two years, a smoother transition into homeownership, and sometimes seller-funded help at closing. But the loan itself is not getting permanently cheaper. The note rate stays the same. The lender still underwrites you at the full payment. And if your budget only works because of the temporary subsidy, the buydown can turn into a delayed affordability problem instead of a solution.

This guide explains what a 2-1 buydown really is, how much it can save in a realistic 2026 example, who usually pays for it, and when it can genuinely help a Florida buyer instead of just making year one look easier.

For related reading, see our Florida first-time homebuyer cost checklist, seller concessions guide, and closing costs guide for Florida buyers.

Quick Answer

A 2-1 buydown is a temporary payment-reduction structure, not a permanent rate cut. In a typical 2-1 buydown, the borrower pays at an interest rate that is 2 percentage points below the note rate in year one, 1 point below in year two, and then the full note rate from year three onward.

Fannie Mae’s temporary buydown guide and Freddie Mac’s temporary subsidy buydown page both require borrowers to qualify at the full note-rate payment, not the bought-down payment. The note itself still reflects the permanent rate.

For Florida buyers in 2026, a 2-1 buydown can create meaningful early-year breathing room, but the savings are only as good as your plan for the higher payment later.

Key takeaway: A 2-1 buydown changes the timing of your payment burden. It does not remove it.

What is a 2-1 buydown?

A 2-1 buydown is a temporary interest-rate subsidy that lowers the borrower’s effective payment in the first two years of the mortgage.

The note rate does not change. Instead, money is set aside in a separate buydown account and applied over time to cover the difference between the temporary payment and the full payment due under the note.

Fannie Mae’s temporary buydown rule says the mortgage instruments must reflect the permanent payment terms, not the buydown terms. Its related job aid overview explains that the lower early-year payment is created by a lump-sum deposit into a buydown account, with funds released over time to reduce the borrower’s payment.

That is the clean definition to remember:

- the note rate stays the same

- the early payment is temporarily reduced

- the difference is covered by subsidy funds already deposited at closing

A 2-1 buydown is not a free discount. It is a front-loaded payment subsidy that ends.

How does a 2-1 buydown work in Florida in 2026?

The mechanics in Florida are the same as the national agency rules.

In year one, the borrower typically pays at a rate 2 points below the note rate. In year two, the borrower pays at a rate 1 point below the note rate. From year three forward, the borrower pays the full note rate.

Fannie Mae says temporary buydowns are allowed on fixed-rate mortgages and certain ARMs for principal residences and second homes, provided the temporary rate reduction does not exceed 3% and the rate increase does not exceed 1% per year. Freddie Mac’s product page says the initial rate on a temporary subsidy buydown plan may not be more than 3 percentage points below the note rate, the plan may not extend beyond three years, and fixed-rate borrowers must be qualified using payments at the note rate.

That is why the hidden truth about a 2-1 buydown is simple: it changes the timing of the payment burden, not the long-term obligation.

In Florida, where buyers may already be absorbing insurance, tax, and closing-cost pressure, that timing shift can still be useful. But it is only useful if year-three affordability is realistic.

How much can it actually lower the payment?

A 2-1 buydown can lower the payment by hundreds of dollars a month in the first two years, but the exact amount depends on the note rate, loan balance, and amortization term.

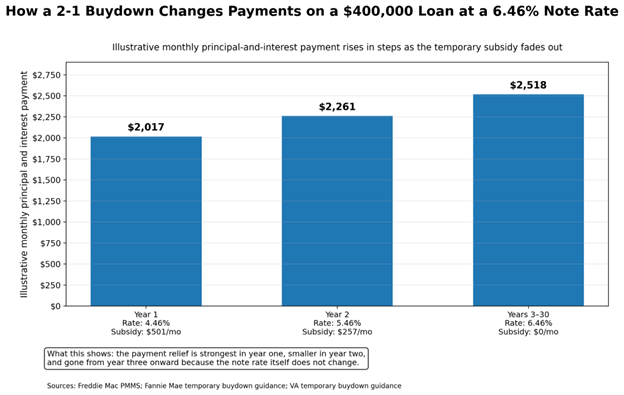

Freddie Mac’s Primary Mortgage Market Survey showed the average 30-year fixed-rate mortgage at 6.46% on April 2, 2026. Using that as an illustration on a $400,000, 30-year fixed mortgage:

- at the full 6.46% note rate, principal and interest is about $2,518/month

- at 4.46% in year one, the illustrative payment is about $2,017/month

- at 5.46% in year two, the illustrative payment is about $2,261/month

That means the payment drops by about:

- $501 per month in year one

- $257 per month in year two

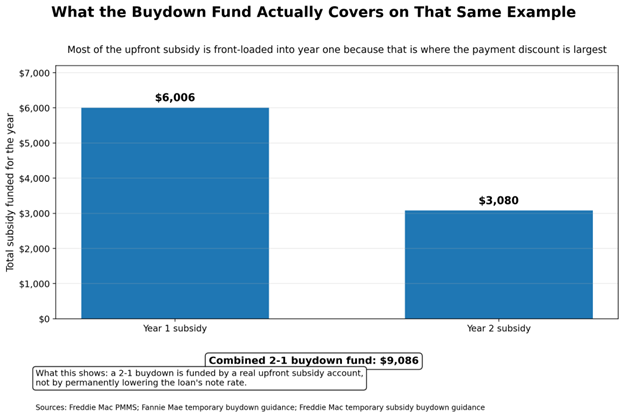

Using standard amortization math, that implies a temporary subsidy of about:

- $6,006 in year one

- $3,080 in year two

- $9,086 total in buydown funds

That is why a 2-1 buydown often feels meaningful at closing: somebody is putting real money into the deal to create those lower early payments.

Who usually funds the buydown?

Who usually funds the buydown?

The buydown can be funded by different parties depending on the loan program and deal structure.

Fannie Mae’s temporary buydown guidance says the funds may come from the borrower, lender, employer, seller, or another interested party. The agency’s temporary buydown requirements job aid also makes clear that these funds must be handled under the program’s specific rules.

For conventional loans sold to Fannie Mae, if the subsidy is funded by an interested party such as the seller or builder, the cost of that subsidy counts toward interested party contribution limits. Fannie Mae says the financing-concession caps for principal residences and second homes are:

- 3% when LTV or CLTV is above 90%

- 6% when LTV or CLTV is 75.01% to 90%

- 9% when LTV or CLTV is 75% or less

For VA loans, the VA temporary buydown page says temporary buydowns can be funded by the seller, lender, builder, or veteran. It also says seller- or builder-funded temporary buydowns count as seller concessions, and seller concessions are capped at 4% of the reasonable value.

In plain English, “seller-funded buydown” does not mean free money floating outside the deal. It is still part of the economics of the transaction, and it still has to be documented properly.

2-1 buydown vs. permanent rate buydown

A 2-1 buydown lowers the payment for a limited early period. A permanent buydown usually means paying discount points to reduce the note rate for the full life of the loan.

The CFPB says points lower the interest rate in exchange for paying more at closing, while lender credits do the reverse by lowering upfront closing costs in exchange for a higher rate.

That means the two strategies solve different problems.

| Feature | 2-1 Buydown | Permanent Rate Buydown |

| What changes | Effective payment for first 2 years | Note rate for the full loan term |

| How it is funded | Subsidy account funded at closing | Usually points paid at closing |

| Qualification | Typically at full note rate | At the actual lower note rate |

| Best for | Buyers wanting short-term payment relief | Buyers expecting to keep the loan longer |

| Main risk | Payment resets higher in year 3 | Higher upfront cash cost |

A 2-1 buydown sits in a different category from points because the note rate stays put and the payment relief is temporary.

When does a 2-1 buydown make sense?

A 2-1 buydown can make sense when the buyer can clearly afford the full payment later, but wants breathing room during the first two years.

The strongest use cases usually look like this:

- the borrower expects reliable income growth

- the household is carrying temporary transition costs

- the buyer wants to preserve liquidity after closing

- the seller or builder is willing to fund the subsidy instead of cutting the price by the same amount

Freddie Mac’s temporary subsidy buydown page describes these plans as a fit for borrowers who have the capacity for higher earnings within a few years and who want lower initial payments with predictable increases.

In Florida, that can matter for buyers trying to keep more cash available after closing for moving costs, repairs, insurance adjustments, or emergency reserves.

If the full payment already works and the temporary savings help you stay liquid, a 2-1 buydown can be a useful tool.

When can a 2-1 buydown backfire?

It can backfire when the buyer focuses on the first-year payment and ignores the permanent payment.

This is exactly why Fannie Mae, Freddie Mac, and VA all emphasize qualification at the full note rate. The rule exists because the temporary payment is not the real long-term burden of the loan.

The biggest risks usually look like this:

- your budget only works because of the year-one payment

- taxes and insurance rise while the buydown is stepping up

- you treat seller credits casually and miss the tradeoff elsewhere in the deal

- you never compare the buydown against a simple price cut or points

There is also a closing-documents issue. The CFPB’s Closing Disclosure explainer says buyers should use the three-day review period before closing to confirm that the loan terms and closing costs are what they expected. If seller credits or lender credits are part of the buydown structure, they should be reviewed carefully on the final forms.

The real risk is not that the buydown malfunctions. The real risk is that the borrower was never comfortable with the full payment to begin with.

What should buyers check on the paperwork?

A buydown should never be treated like a side promise. It needs to show up correctly in the transaction documents.

The CFPB says the Closing Disclosure is the final form that shows your actual loan terms, projected payments, and the fees and other costs required to close your mortgage. The CFPB’s Closing Disclosure page says you must receive it at least three business days before closing.

A strong review should confirm:

- the full note-rate payment

- the year-one and year-two bought-down payments

- who is funding the subsidy

- whether the credit is shown correctly

- whether any seller funding fits within the program limits

- the exact amount of the buydown fund

That review window is where buyers catch surprises while there is still time to ask questions.

Why professional help matters here

A 2-1 buydown sounds simple in conversation, but the real decision is not just “lower payment now or later.”

A mortgage professional can help compare:

- the full note-rate payment

- the bought-down payment path

- a 2-1 buydown versus points

- a 2-1 buydown versus a seller price cut

- a 2-1 buydown versus keeping more cash in reserve

That comparison matters because the cheapest-looking option in year one is not always the smartest option over the next three to five years.

Step-by-step roadmap

The safest way to use a 2-1 buydown is to underwrite your own life the same way the lender underwrites the loan.

- Ask your lender to show the full note-rate payment first.

- Then ask for the year-one and year-two bought-down payments.

- Ask who is funding the subsidy and how it is being treated.

- Compare the 2-1 buydown with a permanent buydown using points.

- Compare it with a plain seller price cut.

- Build your budget around the year-three payment, not the year-one payment.

- Review the Loan Estimate and Closing Disclosure carefully.

- Get the buydown agreement and timing in writing before closing.

Common mistakes

Most 2-1 buydown mistakes are expectation mistakes.

Common examples include:

- confusing a temporary buydown with a permanent rate cut

- budgeting around year one instead of year three

- assuming qualification happens at the lower payment

- ignoring seller-contribution limits

- failing to compare the buydown with points

- treating credits casually on the closing forms

- assuming every lender and loan type handles buydowns the same way

Frequently asked questions

Frequently asked questions

Is a 2-1 buydown the same as paying points?

No. The CFPB says points usually reduce the note rate for the full term of the loan, while a 2-1 buydown temporarily reduces the effective payment for the first two years through a subsidy account.

Do I qualify using the lower payment?

Usually no. Fannie Mae, Freddie Mac, and the VA all say borrowers are qualified using the full note-rate payment, not the temporary bought-down payment.

Who can pay for a seller-funded buydown in Florida?

Depending on the loan program, it may be funded by the seller, builder, lender, borrower, employer, or another eligible party. Program-specific contribution limits still apply.

Is a 2-1 buydown available on investment properties?

Not generally under the mainstream conventional guidance cited here. Fannie Mae and Freddie Mac both limit temporary buydown eligibility to certain occupancy types and product structures.

What happens after the second year?

The subsidy ends and you pay the full note-rate payment from year three onward. That step-up is the central risk buyers need to plan for.

Can unused buydown funds come back to me?

It depends on the program and the agreement. Fannie Mae says lender-funded buydown agreements may provide for remaining funds to be returned if the mortgage pays off early, while the VA says remaining funds on payoff are applied to the outstanding indebtedness.

Why are buydowns getting attention in 2026?

Because rates are still materially above the lows many buyers remember. Freddie Mac’s April 2, 2026 PMMS reading put the average 30-year fixed at 6.46%, which keeps payment-relief strategies in focus.

The bottom line on 2-1 buydowns

A 2-1 buydown can create real short-term savings for Florida buyers in 2026. The hidden value is that it can soften the early payment shock without changing the permanent loan terms.

But the hidden danger is the same thing: it can make a home look more comfortable in year one than it will feel in year three.

The best way to think about a 2-1 buydown is not as a cheaper mortgage, but as a structured transition tool. It can work well when the full payment is already affordable and the temporary relief helps preserve cash or smooth a life change.

Stop guessing. Before you commit, compare the full note-rate payment, the temporary subsidy, the seller-credit structure, and the year-three payment side by side. That is the fastest way to tell whether the hidden savings are real for your situation.

If you want help modeling a 2-1 buydown against points or a plain seller price cut, contact a Pegasus mortgage professional for a no-obligation review.

Sources & References

- Freddie Mac — Primary Mortgage Market Survey (PMMS)

https://www.freddiemac.com/pmms - Fannie Mae — Temporary Interest Rate Buydowns

https://selling-guide.fanniemae.com/sel/b2-1.4-04/temporary-interest-rate-buydowns - Fannie Mae — Overview of Temporary Buydown (Job Aid)

https://singlefamily.fanniemae.com/job-aid/loan-delivery/topic/overview_of_temp_buydown.htm - Fannie Mae — Temporary Buydown Requirements (Job Aid)

https://singlefamily.fanniemae.com/job-aid/loan-delivery/topic/temporary_buydown_requirements.htm - Fannie Mae — Interested Party Contributions (IPCs)

https://selling-guide.fanniemae.com/sel/b3-4.1-02/interested-party-contributions-ipcs - Freddie Mac — Mortgages with Temporary Subsidy Buydown Plans

https://sf.freddiemac.com/working-with-us/origination-underwriting/mortgage-products/mortgages-with-temporary-subsidy-buydown-plans - VA Home Loans — Temporary Buydowns

https://www.benefits.va.gov/homeloans/temporary-buydown.asp - VA Lenders Handbook, Chapter 7 — Loans Requiring Special Underwriting, Guaranty or Other Considerations

https://www.benefits.va.gov/WARMS/docs/admin26/m26-07/chapter_7_loans_requiring_special_underwriting_guaranty_or_other_considerations.pdf - Consumer Financial Protection Bureau — How should I use lender credits and points?

https://www.consumerfinance.gov/ask-cfpb/how-should-i-use-lender-credits-and-points-also-called-discount-points-en-136/ - Consumer Financial Protection Bureau — Closing Disclosure Explainer

https://www.consumerfinance.gov/owning-a-home/closing-disclosure/ - Consumer Financial Protection Bureau — What is a Closing Disclosure?

https://www.consumerfinance.gov/ask-cfpb/what-is-a-closing-disclosure-en-1983/ - Consumer Financial Protection Bureau — TILA-RESPA Integrated Disclosure FAQs

https://www.consumerfinance.gov/compliance/compliance-resources/mortgage-resources/tila-respa-integrated-disclosures/tila-respa-integrated-disclosure-faqs/